'/%3e%3cpath%20d='M4.94162%205.99547L4.02701%205.08086L3.63428%205.47359L4.94162%206.78093L7.63768%204.08487L7.24495%203.69214L4.94162%205.99547Z'%20fill='white'/%3e%3cdefs%3e%3clinearGradient%20id='paint0_linear_2302_10195'%20x1='0.5'%20y1='10'%20x2='10.4939'%20y2='10'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%234E10FF'/%3e%3cstop%20offset='1'%20stop-color='%23AB17DF'/%3e%3c/linearGradient%3e%3c/defs%3e%3c/svg%3e)

If you're in LatAm and your salary is in pesos, bolivars, or any currency that melts faster than ice cream in summer, I’ve got news for you: you needed to dollarize yesterday. This isn’t snobbery. It’s financial survival.

Inflation in Argentina exceeds 200% annually. In Venezuela, it’s even worse. Keeping your savings in local currency is like leaving them in an account with a negative interest rate of -15% per month. Every month that passes, you can buy fewer things with the same stack of bills.

But careful: dollarizing does NOT mean putting USD under your mattress and sitting there waiting. That move is for beginners. Physical dollars don’t generate anything. In fact, with US inflation (which is low, but real), you lose purchasing power year after year. If your horizon is long term, you need that money to work for you.

Why dollarizing is your basic shield

Think of it like this: in a game, if there’s a monster hitting you for -15% health every turn, do you just stand there? No. You look for a shield. The dollar is that shield in inflationary economies. It protects you from the base damage.

But here’s the master move: the shield only protects you, it doesn’t win the game. To win you need offense. And offense means appreciating assets: stocks, Bitcoin, gold, ETFs.

If your horizon is 5+ years, holding USD without investing is wasting a massive opportunity. Historically, S&P 500 stocks have returned around ~10% annually in dollars. Bitcoin has had crazy years (both up and down) but over long periods it has outperformed almost everything. Gold isn’t as flashy, but it’s the reliable friend that’s always there.

How to dollarize from LatAm (without losing your mind)

1. Get the dollars:

- Crypto → USD Coin (USDC) or Tether (USDT) on exchanges like Binance, Bitso, Lemon, Ripio

- P2P → Platforms like AirTM, Reserva, LocalBitcoins

- Informal exchange desks → If you’re in Argentina, you know what this means

- Transferwise/Payoneer → For freelancers paid from abroad

2. Don’t let them sit idle:

If your horizon is short (less than 1 year): stablecoins in crypto platforms with yield (6–12% annually in USDC/USDT).

If your horizon is long (5+ years): buy assets that appreciate.

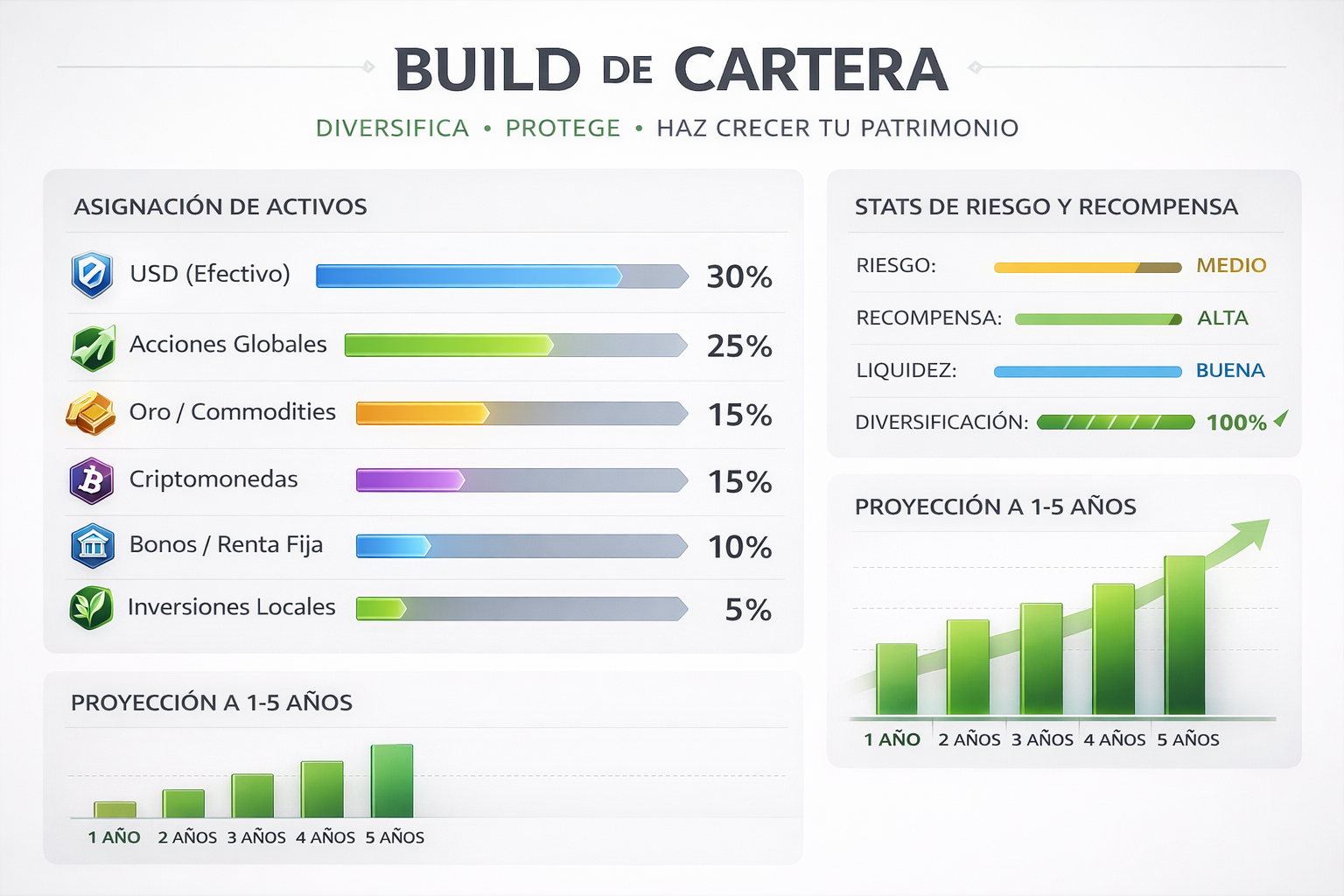

3. Diversify like a character build:

- 60% global stocks (S&P 500 ETF like VOO, or fractional shares in apps like eToro)

- 20% Bitcoin (volatile but huge long-term potential)

- 10% gold (the tank that never fails)

- 10% liquid stablecoins (in case you need cash quickly)

Why smart people don’t leave USD sitting still

Here’s the part that separates the winners from the spectators. Money that isn’t working slowly evaporates. Dollar inflation is about 3–4% annually. If you keep USD in cash, in 10 years you’ve lost 30–40% of your purchasing power.

But if you invest it long term, the game changes:

- $1000 under the mattress in 10 years = purchasing power of ~$700

- $1000 in the S&P 500 in 10 years = ~$2600 (assuming historical returns)

- $1000 in Bitcoin in 10 years = who knows, but historically it’s been wild

The key is starting small and being consistent. You don’t need $10,000 to start investing. With $50–100 per month you’re already playing the game. And when corrections happen (Bitcoin drops 30%, the S&P falls 10%), long-term thinkers celebrate: they’re buying cheaper.

Don Roi’s lesson

1. Spend less than you earn. If you can’t spend less, then you need to earn more.

2. Save and invest FIRST every month, before anything else.

3. Increase that percentage over time. Goal: 10–20% of your income.

4. With the rest: live. Life moves fast.

Tip of the week

Open an account on a crypto platform (Binance, Lemon, Ripio) and buy $20 in USDC or Bitcoin. Just $20. Don’t keep it theoretical. Make it real. Feel what it’s like to hold an asset that doesn’t melt with inflation. Then do it every month. In a year you’ll have $240 + returns + the most important habit of your financial life.

Numbers don’t lie: inflation steals from you quietly, but only if you allow it.

1

0

NEWSLETTER

Subscribe!

And find out the latest news